What Are We Lookin' At?

The S&P 500 enjoyed its biggest bounce in 46 years last week. Which followed the biggest/fastest drop from an all-time high since, well, ever. So, naturally, the question now becomes, where do we go from here?

Markets cheered the Fed's sledgehammer response this past week. To be sure, the monetary and fiscal efforts have been staggering, awe inspiring, and/or jaw dropping. As in, HOW MUCH did they say they would spend again? As in, "Is this on top of everything else?" And as in, "Wait, the Fed is going to buy WHAT!?!"

My colleague Jeff Pietsch, CFA calculates that the combined governmental support (Fed plus Congress) to the economy means spending will be north of $6 trillion - and perhaps as much as $7 trillion. And this is before the "next round" of stimulus occurs. Impressive!

Both the Fed and Congressional responses have been fast and exceeded expectations. And in short, the Fed has effectively taken the scariest scenario off the table - aka another credit crisis. The Fed's buying of not only "fallen angels" but also junk bond ETFs (via a joint effort with Treasury) was an eye-opener. And the recent chatter about venturing into stock ETFs has to strike fear in the hearts of short sellers everywhere.

As a result, the junkiest part of the bond market surged. Stocks that have been bludgeoned spiked in the other direction. And the mean-reversion joyride to the upside was on.

A Trillion Here, A Trillion There...

Before I continue, I'd like to take a moment to try to put the sum of money being created and spent into perspective. So the question is, how much is a trillion dollars anyway? Here's one way to look at it. If you spent $1.3 million each DAY since Jesus died, you still would not have spent even $1 trillion!

Lest we forget, the government was already going to run a deficit of more than $1 trillion this fiscal year. And this is before the additional $6-7 trillion in coronavirus support.

As long as we're talking big numbers, it is also worth remembering that the US economy was approximately $21.4 trillion last year. So, spending 25-30% of that to keep things from falling apart at the seams is certainly reasonable, don't you think?

Stocks basically cheered the plan this week. The idea that throwing trillions at the problem will put some sort of floor under the decline/damage certainly makes sense. Kudos.

In addition, it can be argued that stocks are getting comfortable with the current situation. You know, a decline of 30% in GDP (oh wait, this just in, JPMorgan has taken the lead in the GDP guesstimate derby by moving their Q2 estimate from -24% to -40%), unemployment at 15%, earnings dropping 15% - and then looking ahead to better days. Apparently MUCH better days.

What Are You Lookin' At?

But here's the rub. What exactly are we looking at here? Cutting to the chase, how does the economy "return to normal?"

From my seat, the short answer is, it can't. Not unless the virus just dies and doesn't come back - or a drug cure is found in the next few weeks. As Dr. Fauci has said, this won't be like flipping a switch. There is simply too much change and uncertainty for things to simply go "back to normal."

So, we will be dealing with yet another "new normal." Does anybody know what that looks like in terms of GDP and/or EPS for the SPX? I certainly don't.

For example, what about the appropriate multiple for a market where growth isn't happening?

Think about it. Can we get broad-based growth from this environment? Will Apple sell more phones/watches going forward? Will Starbucks sell more coffee than last year? Will the restaurants that make it through operate anywhere near their pre-virus levels?

Sure, Netflix (NFLX) and Disney (DIS) could see subscriber growth. And word is that gaming is on the rise. Oh and anybody that delivers stuff to the consumer's doorstep should see some good growth. But very large swaths of the economy won't.

Consumer behavior will change. Discretionary spending will drop - at least for a while. Saving for a rainy day/pandemic might even be in vogue.

We can look to China as some sort of a guide here. According to Barron's, "Possible hints of a postcoronavirus world have started to surface... Two and half months since China's lockdowns, people are venturing out: Sales at China's malls have recovered to about half of last year's levels, and home sales are rebounding."

Half of last year's levels. Ouch. Yes, I understand that it's early in the rebound game. But my point here is that "half" is a long way from "normal!"

I don't mean to be a Debbie Downer here. But I keep coming back to the same question week after week. How exactly do we go back to normal until a vaccine is available to the masses? (Assuming the virus doesn't just magically disappear, of course.)

We've Enjoyed A Nice Bounce

So... Stocks have enjoyed a nice bounce. A bounce that so far at least, has followed the crash playbook to the letter. As I have written a time or twenty, after a panic low, some good news emerges that creates a "sigh of relief" or "dead cat" bounce. These rallies tend to take your breath away and give you the feeling that everything is all better now. Check.

And yes, retracing 50% of the initial decline is perfectly normal, which is exactly what we had in the early going on Thursday.

But according to the playbook, reality is about to set in. This is where "the original reason for the decline resurfaces." Presently, this could take the form of the "reality" that the economy isn't going to spring right back to normal. Or that savings becomes cool again. Or that parents aren't going to let kids play soccer, participate in plays or chorus, or even visit Grandma anytime soon. We just don't know when or if "normal" stuff resumes again.

Also note that this "reality check" doesn't have to happen immediately. Perhaps stocks can continue to look ahead, to look past the current nadir, and to better days for some time yet. Some additional "feel good" news could easily push stocks higher still.

Until/unless a second wave of the virus hits and we are forced to shut everything down again. But I'll stop that train of thought right there. As a "glass is half-full" kinda guy, I simply don't want to go there.

My point is that those looking for an immediate V-Bottom in the stock market may be disappointed. Yes the government is to be applauded for their efforts to stem the tide. Yes, spending $6-7 trillion will help. But it won't get things back to normal. And it won't create widespread growth.

Because of this (and this is my big point this morning), I think we need to recognize that there is a limit to how far the current joyride to the upside can run.

From my seat the market will have to deal with economic "reality" at some point. And from some price level. Because you can't put a growth multiple on a market where the economy is struggling.

But, the Retest Theme is a Crowded Idea

I will admit that FAR too many people are looking for a "retest" in the stock market. This alone gives me pause. You see, I know full well that Ms. Market loves to frustrate the masses. So maybe we don't see a big, bad retest of the lows in the near-term. But maybe we don't see a sprint back to the highs either.

This leaves me with the idea of a prolonged range-bound environment where the range can accommodate multiple "cyclical" bulls/bears (I.E. 20% moves). Remember, these types of moves now occur in a matter of days/weeks, not months.

My thinking is that an extended and wide trading range could afford the market the time and latitude to get comfortable with the "new normal", whatever that may be.

Weekly Market Model Review

Each week we do a disciplined, deep dive into our key market indicators and models. The overall goal of this exercise is to (a) remove emotion from the investment process, (b) stay "in tune" with the primary market cycles, and (c) remain cognizant of the risk/reward environment.

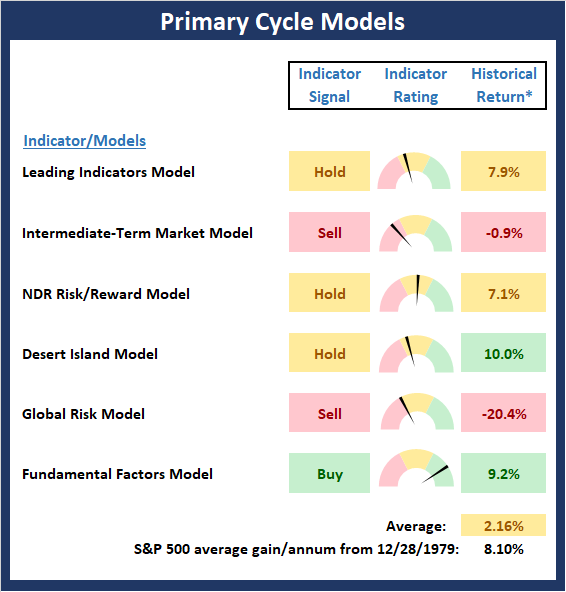

The Major Market Models

We start with six of our favorite long-term market models. These models are designed to help determine the "state" of the overall market.

There is one change to report on the Primary Cycle board this week as my "Desert Island Model" upticked from negative to neutral. With two sell signals, three hold signals, one buy signal, and an average historical return of the market when the models are in their current state of just 2.2%, I'm going to have to rate the board as moderately negative. However, the good news is this rating represents an uptick from the recent negative reading.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability - NOT INDIVIDUAL INVESTMENT ADVICE.

View My Favorite Market Models Online

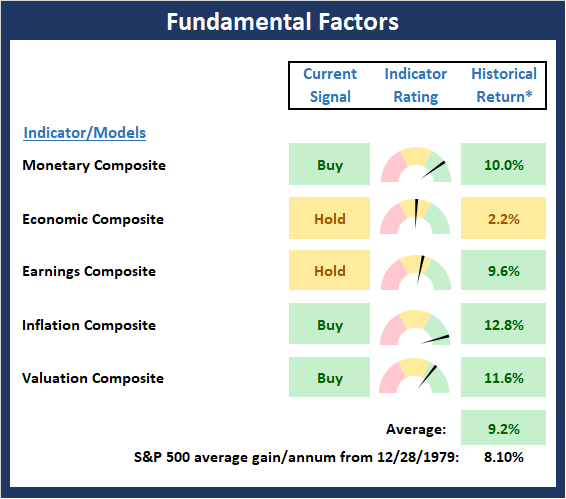

The State of the Fundamental Backdrop

Next, we review the market's fundamental factors in the areas of interest rates, the economy, inflation, and valuations.

There are no changes to report on the Fundamental Factors board this week. As I have been saying, this board is very slow to change and is woefully behind the rapidly deteriorating economic curve at this point. However, the fact that the board was positive before the crisis tells me that there is likely to be meaningful upside when this market makes the turn and moves into a new bull cycle. But for now, it is important to recognize that the green on this board is misleading.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability - NOT INDIVIDUAL INVESTMENT ADVICE.

View Fundamental Indicator Board Online

{kind=link}

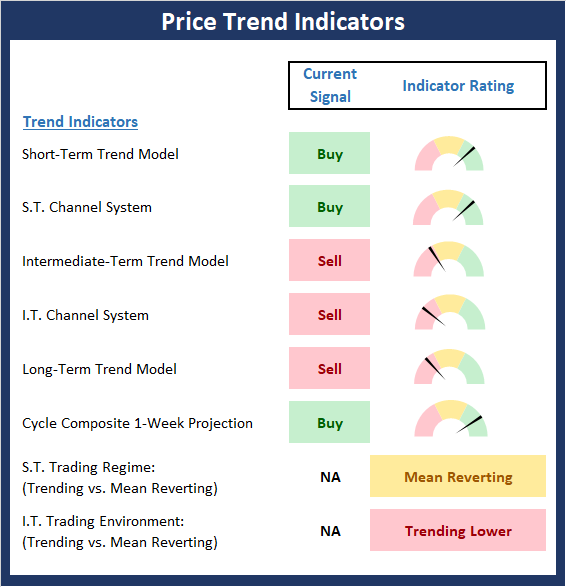

The State of the Trend

After looking at the big-picture models and the fundamental backdrop, I like to look at the state of the trend. This board of indicators is designed to tell us about the overall technical health of the current trend.

After the best week for the S&P 500 since 1974, it isn't surprisingly to see some improvement on the Trend board. Specifically, the short-term trend and channel indicators flipped from red to green. However, there is still some work needed to recover from an intermediate- and longer-term perspective.

NOT INDIVIDUAL INVESTMENT ADVICE.

View Trend Indicator Board Online

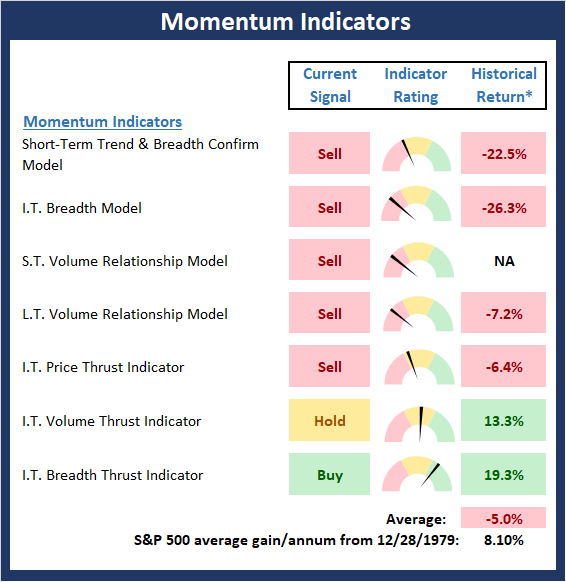

The State of Internal Momentum

Next, we analyze the "oomph" behind the current trend via our group of market momentum indicators/models.

The Momentum Board also saw some improvement this week as our breadth thrust indicator and trend/breadth confirm indicators both moved into the green and the price thrust indicators upticked to neutral. The key to the momentum picture is the time frame one chooses to focus on. From a short-term perspective, momentum is pretty good. But from an intermediate-term perspective, it's a different story.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability - NOT INDIVIDUAL INVESTMENT ADVICE.

View Momentum Indicator Board Online

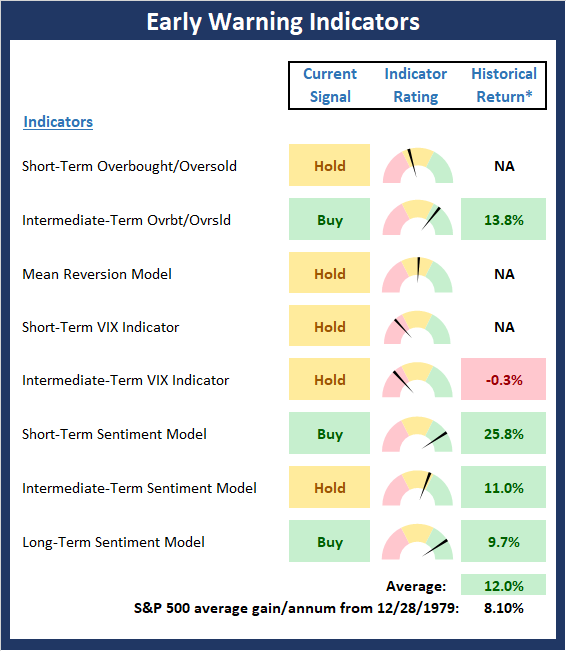

Early Warning Signals

Once we have identified the current environment, the state of the trend, and the degree of momentum behind the move, we then review the potential for a counter-trend move to begin. This batch of indicators is designed to suggest when the table is set for the trend to "go the other way."

The Early Warning board is a bit misleading at this point. While there is a fair amount of green on the board, it again depends on your time frame. From a short-term point of view, stocks are becoming overbought. And while sentiment remains negative (a good thing), the bulls will likely need to take a rest at some point soon.

* Source: Ned Davis Research (NDR) as of the date of publication. Historical returns are hypothetical average annual performances calculated by NDR. Past performances do not guarantee future results or profitability - NOT INDIVIDUAL INVESTMENT ADVICE.

View Early Warning Indicator Board Online

Thought For The Day:

It's not what it's worth, it's where you can sell it. - Bernard Baruch

Wishing you green screens and all the best for a great day,

David D. Moenning

Founder, Chief Investment Officer

Heritage Capital Research

Disclosures

At the time of publication, Mr. Moenning held long positions in the following securities mentioned: JPM, AAPL, NFLX, - Note that positions may change at any time.

Leading Indicators Model: A group of indicators that have historically shown tendencies to lead the market at major turning points.

Intermediate-Term Market Model: A composite model (model of models) focused on trend and momentum indicators which has been designed to provide identify intermediate-term trading opportunities.

Risk/Reward Model: A model-of-models intended to provide an overall view of the state of the risk/reward environment. The model includes tape, monetary, and sentiment indicators as well as 7 big-picture market model readings.

Desert Island Model: If I was stranded on a desert island with access to only one market model to manage money with, this would be the model. The model is a comprehensive model-of-models comprised of trend, momentum, mean reversion, economic, monetary, sentiment, and factor-based indicators/models.

External Factors Model: A model-of-models designed to provide a reading on the "macro state" of the market environment. The model is comprised of indicators/models in the areas of various index yields, industrial production, investors sentiment, and historic volatility.

Short-Term Trend-and-Breadth Signal Explained: History shows the most reliable market moves tend to occur when the breadth indices are in gear with the major market averages. When the breadth measures diverge, investors should take note that a trend reversal may be at hand. This indicator incorporates NDR's All-Cap Dollar Weighted Equity Series and A/D Line. From 1998, when the A/D line is above its 5-day smoothing and the All-Cap Equal Weighted Equity Series is above its 25-day smoothing, the equity index has gained at a rate of +32.5% per year. When one of the indicators is above its smoothing, the equity index has gained at a rate of +13.3% per year. And when both are below, the equity index has lost +23.6% per year.

Channel Breakout System Explained: The short-term and intermediate-term Channel Breakout Systems are modified versions of the Donchian Channel indicator. According to Wikipedia, "The Donchian channel is an indicator used in market trading developed by Richard Donchian. It is formed by taking the highest high and the lowest low of the last n periods. The area between the high and the low is the channel for the period chosen."

Intermediate-Term Trend-and-Breadth Signal Explained: This indicator incorporates NDR's All-Cap Dollar Weighted Equity Series and A/D Line. From 1998, when the A/D line is above its 45-day smoothing and the All-Cap Equal Weighted Equity Series is above its 45-day smoothing, the equity index has gained at a rate of +17.6% per year. When one of the indicators is above its smoothing, the equity index has gained at a rate of +6.5% per year. And when both are below, the equity index has lost -1.3% per year.

Cycle Composite Projections: The cycle composite combines the 1-year Seasonal, 4-year Presidential, and 10-year Decennial cycles. The indicator reading shown uses the cycle projection for the upcoming week.

Trading Mode Indicator: This indicator attempts to identify whether the current trading environment is "trending" or "mean reverting." The indicator takes the composite reading of the Efficiency Ratio, the Average Correlation Coefficient, and Trend Strength models.

Volume Relationship Models: These models review the relationship between "supply" and "demand" volume over the short- and intermediate-term time frames.

Price Thrust Model Explained: This indicator measures the 3-day rate of change of the Value Line Composite relative to the standard deviation of the 30-day average. When the Value Line's 3-day rate of change have moved above 0.5 standard deviation of the 30-day average ROC, a "thrust" occurs and since 2000, the Value Line Composite has gained ground at a rate of +20.6% per year. When the indicator is below 0.5 standard deviation of the 30-day, the Value Line has lost ground at a rate of -10.0% per year. And when neutral, the Value Line has gained at a rate of +5.9% per year.

Volume Thrust Model Explained: This indicator uses NASDAQ volume data to indicate bullish and bearish conditions for the NASDAQ Composite Index. The indicator plots the ratio of the 10-day total of NASDAQ daily advancing volume (i.e., the total volume traded in stocks which rose in price each day) to the 10-day total of daily declining volume (volume traded in stocks which fell each day). This ratio indicates when advancing stocks are attracting the majority of the volume (readings above 1.0) and when declining stocks are seeing the heaviest trading (readings below 1.0). This indicator thus supports the case that a rising market supported by heavier volume in the advancing issues tends to be the most bullish condition, while a declining market with downside volume dominating confirms bearish conditions. When in a positive mode, the NASDAQ Composite has gained at a rate of +38.3% per year, When neutral, the NASDAQ has gained at a rate of +13.3% per year. And when negative, the NASDAQ has lost at a rate of -14.279% per year.

Breadth Thrust Model Explained: This indicator uses the number of NASDAQ-listed stocks advancing and declining to indicate bullish or bearish breadth conditions for the NASDAQ Composite. The indicator plots the ratio of the 10-day total of the number of stocks rising on the NASDAQ each day to the 10-day total of the number of stocks declining each day. Using 10-day totals smooths the random daily fluctuations and gives indications on an intermediate-term basis. As expected, the NASDAQ Composite performs much better when the 10-day A/D ratio is high (strong breadth) and worse when the indicator is in its lower mode (weak breadth). The most bullish conditions for the NASDAQ when the 10-day A/D indicator is not only high, but has recently posted an extreme high reading and thus indicated a thrust of upside momentum. Bearish conditions are confirmed when the indicator is low and has recently signaled a downside breadth thrust. In positive mode, the NASDAQ has gained at a rate of +22.1% per year since 1981. In a neutral mode, the NASDAQ has gained at a rate of +14.5% per year. And when in a negative mode, the NASDAQ has lost at a rate of -6.4% per year.

Short-Term Overbought/sold Indicator: This indicator is the current reading of the 14,1,3 stochastic oscillator. When the oscillator is above 80 and the %K is above the %D, the indicator gives an overbought reading. Conversely, when the oscillator is below 20 and %K is below its %D, the indicator is oversold.

Intermediate-Term Overbought/sold Indicator: This indicator is a 40-day RSI reading. When above 57.5, the indicator is considered overbought and wnen below 45 it is oversold.

Mean Reversion Model: This is a diffusion model consisting of five indicators that can produce buy and sell signals based on overbought/sold conditions.

VIX Indicator: This indicators looks at the current reading of the VIX relative to standard deviation bands. When the indicator reaches an extreme reading in either direction, it is an indication that a market trend could reverse in the near-term.

Short-Term Sentiment Indicator: This is a model-of-models composed of 18 independent sentiment indicators designed to indicate when market sentiment has reached an extreme from a short-term perspective. Historical analysis indicates that the stock market's best gains come after an environment has become extremely negative from a sentiment standpoint. Conversely, when sentiment becomes extremely positive, market returns have been subpar.

Intermediate-Term Sentiment Indicator: This is a model-of-models composed of 7 independent sentiment indicators designed to indicate when market sentiment has reached an extreme from a intermediate-term perspective. Historical analysis indicates that the stock market's best gains come after an environment has become extremely negative from a sentiment standpoint. Conversely, when sentiment becomes extremely positive, market returns have been subpar.

Long-Term Sentiment Indicator: This is a model-of-models composed of 6 independent sentiment indicators designed to indicate when market sentiment has reached an extreme from a long-term perspective. Historical analysis indicates that the stock market's best gains come after an environment has become extremely negative from a sentiment standpoint. Conversely, when sentiment becomes extremely positive, market returns have been subpar.

Absolute Monetary Model Explained: The popular cliche, "Don't fight the Fed" is really a testament to the profound impact that interest rates and Fed policy have on the market. It is a proven fact that monetary conditions are one of the most powerful influences on the direction of stock prices. The Absolute Monetary Model looks at the current level of interest rates relative to historical levels and Fed policy.

Relative Monetary Model Explained: The "relative" monetary model looks at monetary indicators relative to recent levels as well as rates of change and Fed Policy.

Economic Model Explained: During the middle of bull and bear markets, understanding the overall health of the economy and how it impacts the stock market is one of the few truly logical aspects of the stock market. When our Economic model sports a "positive" reading, history (beginning in 1965) shows that stocks enjoy returns in excess of 21% per year. Yet, when the model's reading falls into the "negative" zone, the S&P has lost nearly -25% per year. However, it is vital to understand that there are times when good economic news is actually bad for stocks and vice versa. Thus, the Economic model can help investors stay in tune with where we are in the overall economic cycle.

Inflation Model Explained: They say that "the tape tells all." However, one of the best "big picture" indicators of what the market is expected to do next is inflation. Simply put, since 1962, when the model indicates that inflationary pressures are strong, stocks have lost ground. Yet, when inflationary pressures are low, the S&P 500 has gained ground at a rate in excess of 13%. The bottom line is inflation is one of the primary drivers of stock market returns.

Valuation Model Explained: If you want to get analysts really riled up, you need only to begin a discussion of market valuation. While the question of whether stocks are overvalued or undervalued appears to be a simple one, the subject is actually extremely complex. To simplify the subject dramatically, investors must first determine if they should focus on relative valuation (which include the current level of interest rates) or absolute valuation measures (the more traditional readings of Price/Earnings, Price/Dividend, and Price/Book Value). We believe that it is important to recognize that environments change. And as such, the market's focus and corresponding view of valuations are likely to change as well. Thus, we depend on our Valuation Models to help us keep our eye on the ball.

Disclosures

NOT INVESTMENT ADVICE. The opinions and forecasts expressed herein are those of Mr. David Moenning and Heritage Capital Research and may not actually come to pass. The opinions and viewpoints regarding the future of the markets should not be construed as recommendations. The analysis and information in this report is for informational purposes only. No part of the material presented in this report is intended as an investment recommendation or investment advice. Neither the information nor any opinion expressed constitutes a solicitation to purchase or sell securities or any investment program.

Any investment decisions must in all cases be made by the reader or by his or her investment adviser. Do NOT ever purchase any security without doing sufficient research. There is no guarantee that the investment objectives outlined will actually come to pass. All opinions expressed herein are subject to change without notice. Neither the editor, employees, nor any of their affiliates shall have any liability for any loss sustained by anyone who has relied on the information provided.

Mr. Moenning of Heritage Capital Research is an investment adviser representative of Eastsound Capital Advisors, LLC, a registered investment advisor. The adviser may not transact business in states where it is not appropriately registered, excluded or exempted from registration. Individualized responses to persons that involve either the effecting of transaction in securities, or the rendering of personalized investment advice for compensation, will not be made without registration or exemption.

Mr. Moenning and Heritage Capital Research may at times have positions in the securities referred to and may make purchases or sales of these securities while publications are in circulation. Positions may change at any time.

The analysis provided is based on both technical and fundamental research and is provided "as is" without warranty of any kind, either expressed or implied. Although the information contained is derived from sources which are believed to be reliable, they cannot be guaranteed.

The author neither endorses nor warrants the content of this site, any embedded advertisement, or any linked resource. The author or his managed funds may hold either long or short positions in the referenced securities. Republication rights must be expressly granted by author in writing.

Investments in equities carry an inherent element of risk including the potential for significant loss of principal. Past performance is not an indication of future results.